A recent article posted at the Santa Fe New Mexican (SFNM), “Climate change and the coming real estate calamity,” claims that climate change is causing an increase in extreme and damaging weather, which then causes homes to be uninsurable. [emphasis, links added]

This is false. There has been no increase in extreme weather alongside the modest warming of the past century.

The SFNM warns ominously that climate change could cause so much property damage and loan defaults that the banking system will suffer worse than it did during the 2008 crisis.

The cause of this housing calamity: climate change will make “millions of homes uninsurable or unfinanceable,” because global warming “is causing a rapid increase in extreme weather.”

As evidence of this alleged scientific claim, the post points to the devastating fires in Los Angeles this past January, which destroyed 18,000 homes, and Hurricane Helene, which caused destruction across multiple states.

While it is true that weather events like massive wildfires and hurricanes are highly destructive to life and property, it is not true that climate change is making them more severe or frequent.

In the case of the Los Angeles fires, a man was just arrested on arson charges for having intentionally started the blaze. So the origin of the fire was not natural. Local weather conditions did not help any—dry grasses and high Santa Ana winds created a perfect storm for spreading fire quickly.

That dryness was not part of any long-term trend, as explained in this Climate Realism post here, but rather was a reflection of a single, natural, unseasonably dry winter.

Los Angeles has actually seen an increase in precipitation for their winter season over time; this past year was an anomaly that cannot be attributed to long-term climate change.

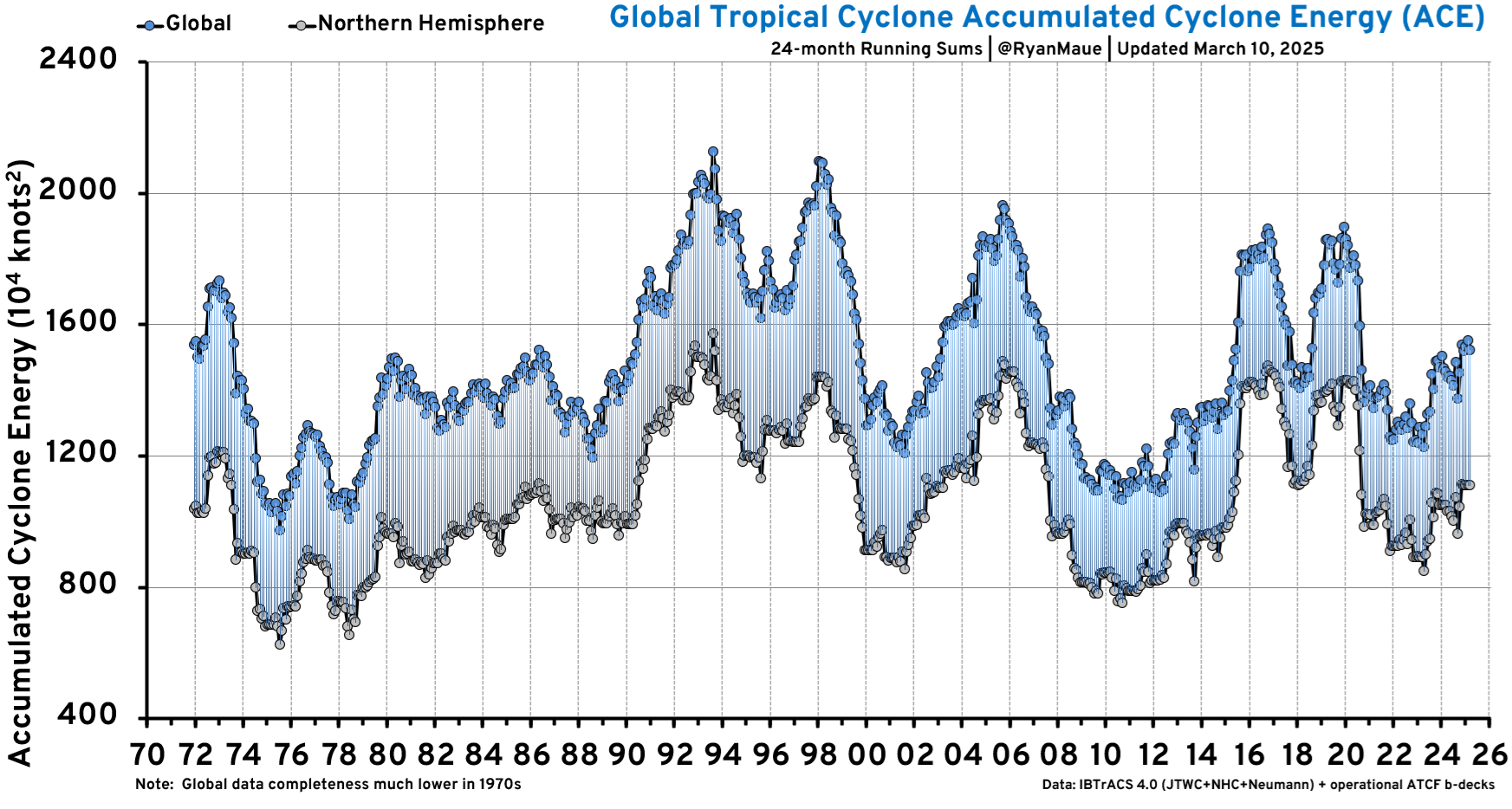

Similarly, Hurricane Helene was not unprecedented, nor was it part of a long-term trend of worsening hurricanes. Climate Realism has covered the hurricane issue many times, including several posts on Helene alone, which was unquestionably devastating, especially for North Carolina.

But again, as with those previous analyses, hurricanes have not experienced a long-term trend of more frequent or powerful hurricanes that could be attributed to the warming of the past hundred-plus years.

Actual data on hurricanes, such as the global tropical accumulated cyclone energy (ACE) data, presented below by Dr. Ryan Maue, show no persistent trend in hurricane severity either globally or in the northern hemisphere. (See figure below)

Storms and wildfires today are causing more damage and [incurring higher costs than they did] in the past, not due to worsening storms or wildfires, but rather from population growth in areas prone to hurricanes and wildfires, accompanied by [the construction of more expensive homes and structures].

When there’s more to destroy and the property involved is more valuable, [the cost of destruction naturally increases, especially during hurricanes or wildfires].

Despite this fact, global weather losses as a percent of GDP have declined over time, with economic growth exceeding losses when adjusted for inflation. (see figure below)

If extreme weather is not getting worse, insurance premiums can’t be increasing as a result of worsening weather, nor can insurer withdrawals from certain neighborhoods be blamed on more imaginary severe storms.

Increasing populations in naturally disaster-prone areas, inflation, and government policies towards insurance companies and subsidies are the real factors driving rising insurance costs and insurers dropping out of some areas.

It is convenient for insurance companies to blame climate change because it is forever just over the horizon and can be used to intimidate customers into not complaining about higher rates.

The SFNM business section should not be carrying water for these profiteers. The data simply doesn’t support a climate change connection to the actions of the insurance industry.

Top image by Dirk (Beeki®) Schumacher from Pixabay

Read more at Climate Realism

{kind=link}